at Free Money Finance")

Update: Voting is now closed. We won and are into the second round. Thanks everyone!

A month into 2009 and the bad news continues. Perhaps I’m becoming immune to the economic gloom or maybe it’s the first sign of spring, but I can’t help feeling we should look on the bright side.

A month into 2009 and the bad news continues. Perhaps I’m becoming immune to the economic gloom or maybe it’s the first sign of spring, but I can’t help feeling we should look on the bright side.

Yes, the world economy is undergoing a severe contraction. Millions of people are losing their jobs, and investors have seen their long-term equity holdings halve or worse in value. Even countries such as Iceland are going bankrupt.

But you know what? It could be worse.

The universally pessimistic financial commentary might have been useful in 2007, when investors could try to do something about it. But with a few honorable exceptions, everyone expected those debt-fueled good times to last forever. Banks lent huge amounts against inflated property values on the grounds that prices wouldn’t ever fall, and politicians like the UK’s Gordon Brown ‘balanced’ their budgets by assuming they’d abolished the boom-and-bust economic cycle.

Busts in capitalist systems happen for a good reason. In the absence of (inefficient) central planning, we need the market to correct the imbalances that build up as people and institutions slowly distort the system.

Something had to be done to stop the poor allocation of capital, whether by ordinary people bidding up the prices of their homes or cynical bankers slicing off millions in bonuses for playing pass-the-parcel with toxic and highly-leveraged assets.

Clearing uncompetitive retailers out of the high street and forcing inefficient companies to shape up or ship out overseas will also be valuable in the long run.

None of this is to diminish the suffering if you’ve lost your job or your home. But from a global perspective, things could be far, far worse.

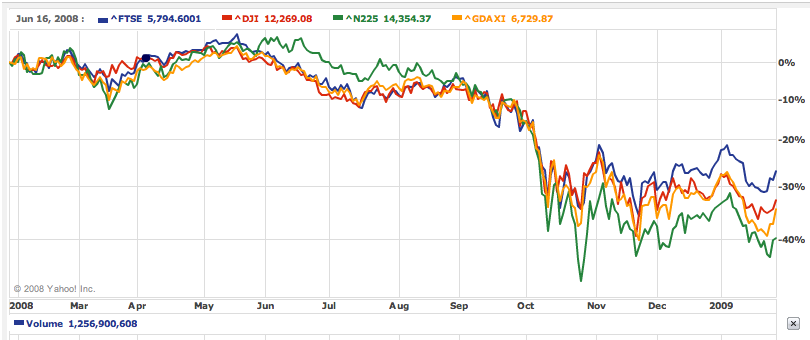

(Source: Yahoo)

Books on investment often suggest investing overseas as a method of diversifying your portfolio. There are several reasons why investing abroad can be a good idea, including:

- If one country or region’s market is doing badly, another could be doing well. Mixing up the returns from several regions helps to smooth the return from your investments.

- Some countries have very different economic profiles to the mature Western regions. In particular, India, China, and other emerging markets are expected to grow much more rapidly, although the journey will be bumpy. Allocating 5-10% of your portfolio to emerging markets enables you to capture some of the growth without suffering too much volatility.

- Currency factors. If you’re an American investor and you invest in European stocks, you will be exposed to the performance of the Euro versus the dollar, as well as the performance of your European stocks. Different currency pairs can diverge a huge amount over time, further diversifying your portfolio – albeit at the cost of extra risk.

Diversifying overseas sounds great in theory. But as the graph at the start of this article shows (click to enlarge), the major world markets have moved in step in recent times.

{kind=link}

Even before the credit crisis, many commentators were saying the world’s markets were becoming closely coupled. Is there any point then in putting money overseas?

Looks like the age of 0% interest rates has come early for customers of TD Waterhouse in the UK, which just announced the rates pictured for cash held in its various share dealing accounts.

Dealing accounts typically offer terrible interest rates on uninvested cash, but 0% is taking the biscuit (or rather all of the interest the uninvested cash generates).

With the price of bank shares being driven by fear, should we avoid them completely? Or if we do want to get specific exposure to banks, which banks look the best?

As a private investor, I can only tell you what I’m doing (and remind you an index tracking fund should underpin your portfolio, not individual stock picks).

My personal view is that bank shares will continue to oscillate wildly until house prices stop falling. Then banks should begin to strengthen.

Further falls in house prices in the UK (which I expect) will hit our banks further, though I suspect the scale is now manageable after their capital raising and/or government injections. Much will depend on the performance of their other debt, such as loans to companies struggling through a recession.

The positive spin is that absent a global economic meltdown causing 30-40% of homeowners to default, any bank that survives the credit crisis will at some point be worth a lot more than today. Assets such as mortgages that were previously written right down will then be revalued upwards. (See my post on Prodesse, the investor in US mortgages).